At SHUAA we are committed to being at the forefront of the latest market trends and providing innovative investment solutions for our clients and stakeholders.

As part of our leading Private Debt practice in the region with over $545M invested, we have collaborated with MAGNiTT and published the 2022 MENA Venture Debt Investment Report.

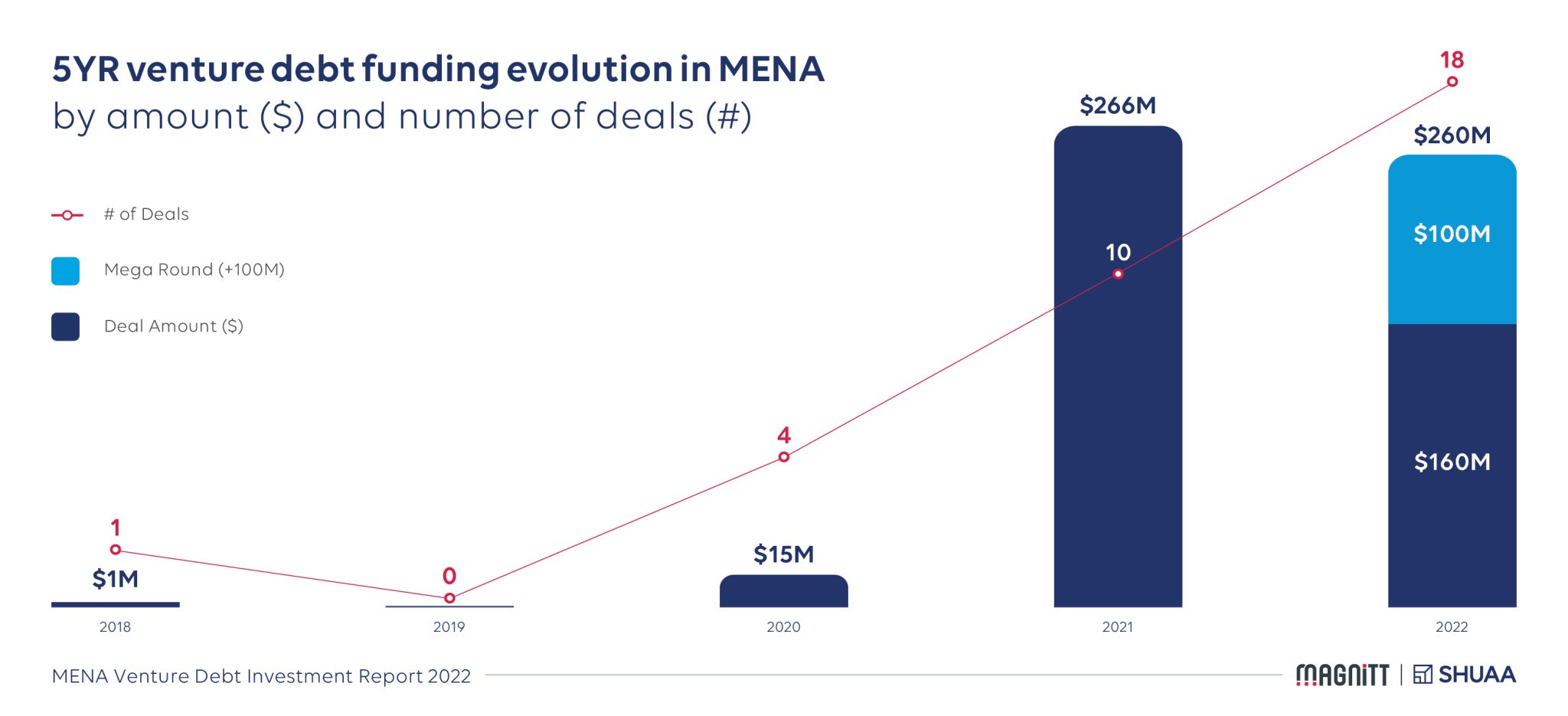

The role of venture debt has been growing in the MENA region over the past five years, with 2021 reporting a record-high funding total. The 18x rise in venture debt funding between 2020 and 2021 highlighted its elevated position as a strategic tool to support startup growth.

Venture debt deals almost doubled between 2021 and 2022, despite total investment in 2022 falling $6M short of the funding in 2021. Venture debt aggregated $260M across 18 deals in 2022, a year that saw the first mega-deal for venture debt in the MENA region. The deal was closed by UAE-based FinTech startup Tabby and contributed 39% to the total venture debt funding reported in 2022.

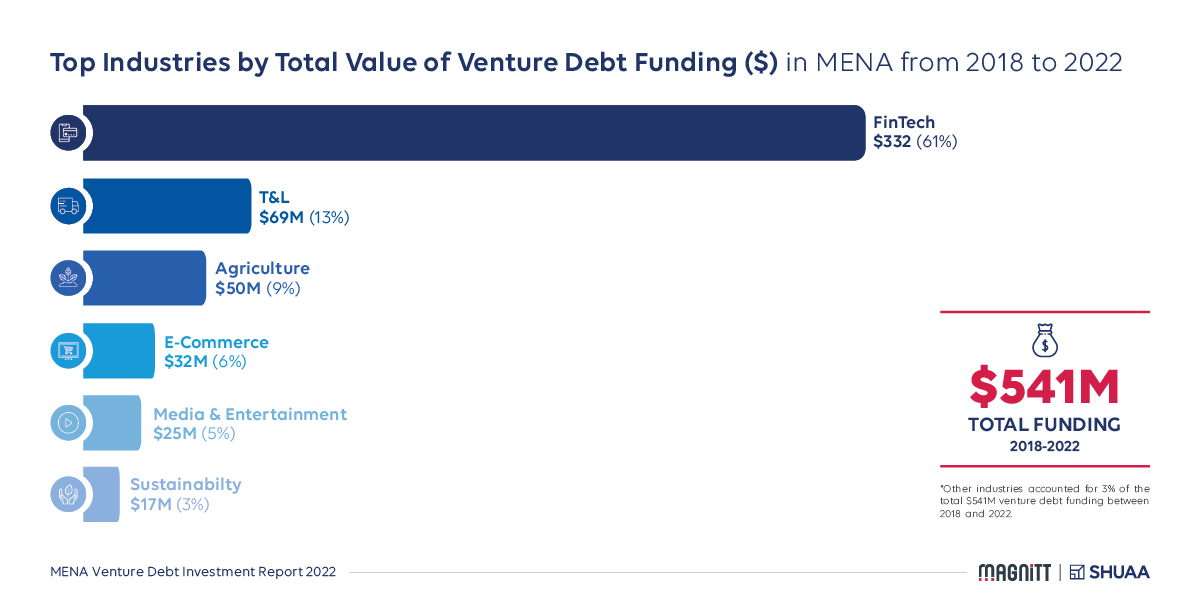

The report maps the evolution of venture debt funding and activity in the Middle East and North Africa (MENA) region over the past five years by target countries, industries and investors.